Grab Reports Fourth Quarter and 2025 Results with First Full Year Net Profit

SINGAPORE, February 12, 2026 – Grab Holdings Limited (NASDAQ: GRAB) today announced unaudited financial results for the fourth quarter ended December 31, 2025.

“We exited 2025 with a record fourth quarter, delivering our first full year of net profit and crossing 50 million Monthly Transacting Users,” said Anthony Tan, Group Chief Executive Officer and Co-Founder of Grab. “We will build on this momentum by executing on a multi-year strategy focused on further expanding our addressable market through greater affordability and reliability, while harnessing product-led innovations to deepen ecosystem engagement and expand user lifetime values.”

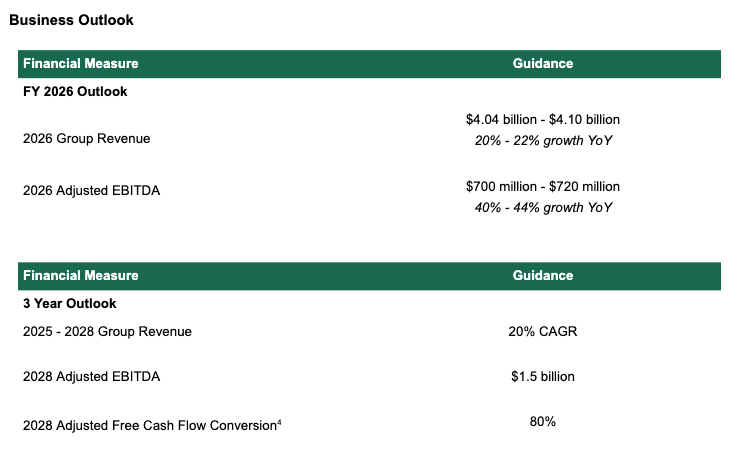

“We delivered another record full year Adjusted Free Cash Flow through disciplined cost management and strengthened unit economics, solidifying our liquidity position and validating our long-term strategy,” said Peter Oey, Chief Financial Officer of Grab. “This strong foundation underpins our confidence in our long-term financial outlook, where we expect to generate $1.5 billion in Adjusted EBITDA with an Adjusted Free Cash Flow conversion of 80% by 2028. This provides us with greater flexibility to accelerate our platform ambitions while delivering shareholder value. To that end, we are announcing a newly authorized $500 million Share Repurchase Program.”

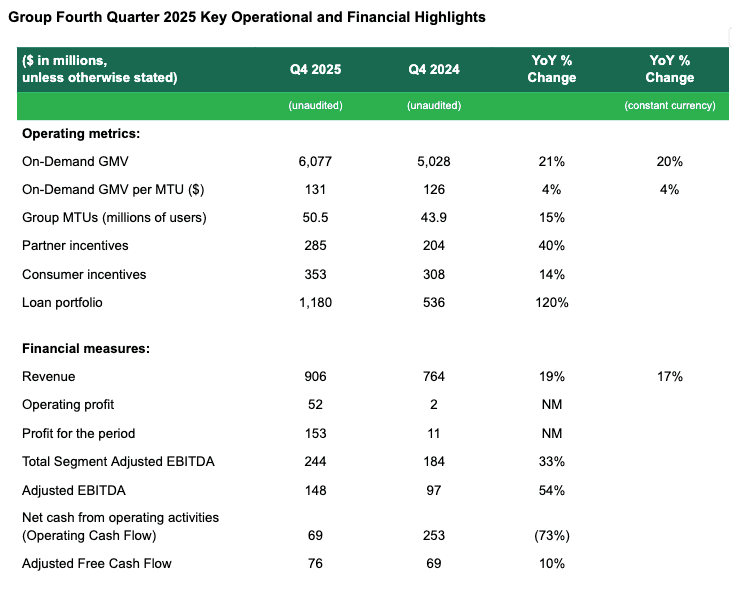

- Revenue grew 19% YoY, or 17% on a constant currency basis to $906 million in the fourth quarter of 2025, driven by growth across our On-Demand and Financial Services segments.

- On-Demand GMV grew 21% YoY, or 20% YoY on a constant currency basis to $6.1 billion, underpinned by strong YoY growth in On-Demand MTUs and total number of On-Demand transactions at 16% and 24% respectively, and a 4% YoY constant currency increase in On-Demand GMV per MTU.

- Total incentives were $638 million during the quarter. On-Demand incentives as a proportion of On-Demand GMV increased by 31bps YoY and 38bps QoQ at 10.4% primarily due to higher seasonal demand in our mobility services that increased our partner incentives.

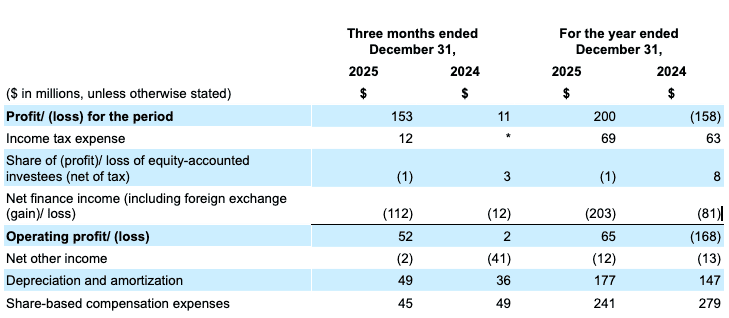

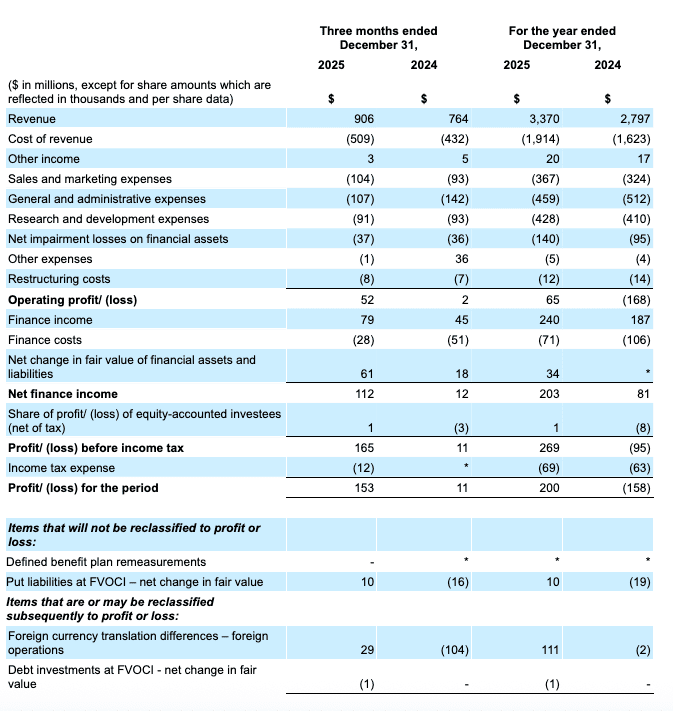

- Operating profit in the fourth quarter was $52 million, an improvement of $50 million YoY, primarily driven by increases in revenue and lower general and administrative expenses.

- Profit for the period was $153 million, an improvement of $142 million YoY, due to increased operating profit and net finance income, partially offset by higher income tax expenses incurred for the period.

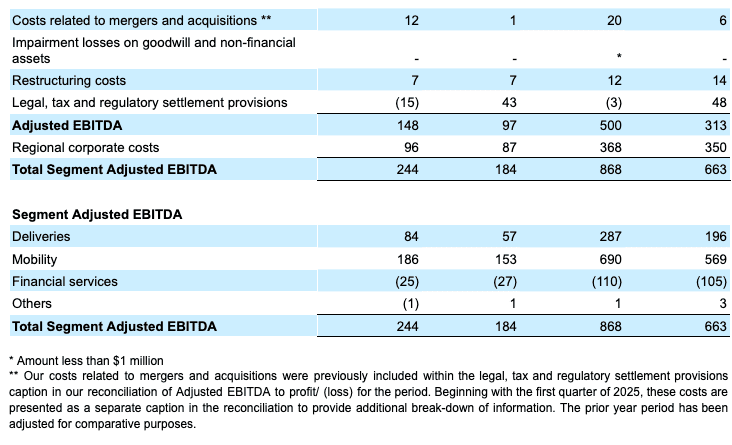

- Adjusted EBITDA was $148 million for the quarter, an improvement of $52 million YoY from $97 million in the prior year period, as we grew On-Demand GMV and revenue, while improving profitability on a Segment Adjusted EBITDA basis.

- Regional corporate costs1 for the quarter were $96 million, an increase compared to $87 million in the prior year period and $95 million in the third quarter of 2025, but an improvement YoY and QoQ as a percentage of revenue as we increased operating leverage.

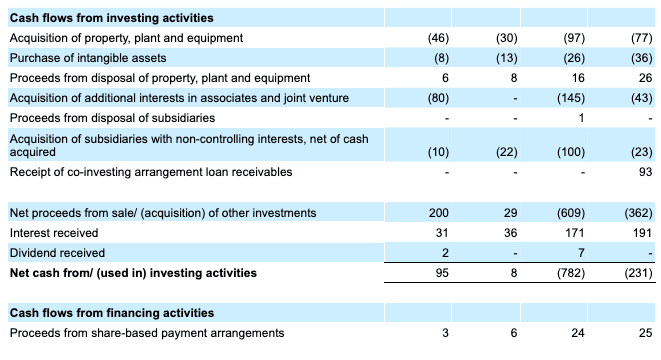

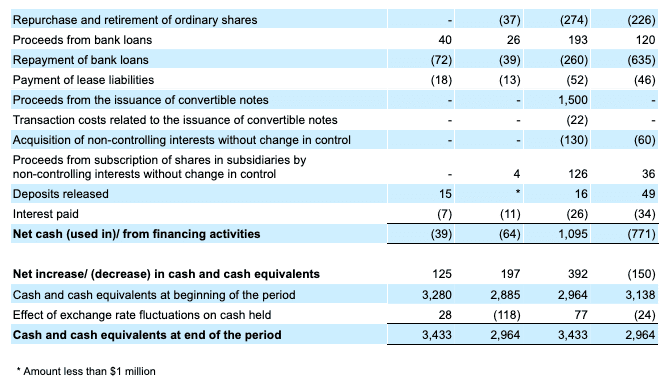

- Gross cash liquidity2 was flat QoQ and totaled $7.4 billion at the end of the fourth quarter, compared to $6.1 billion in the prior year period. Net cash liquidity was $5.4 billion at the end of the fourth quarter, an increase compared to $5.3 billion at the end of the prior quarter primarily due to a reduction in loans and borrowings.

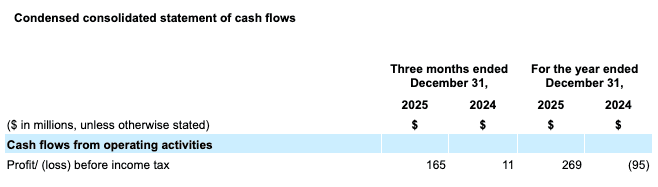

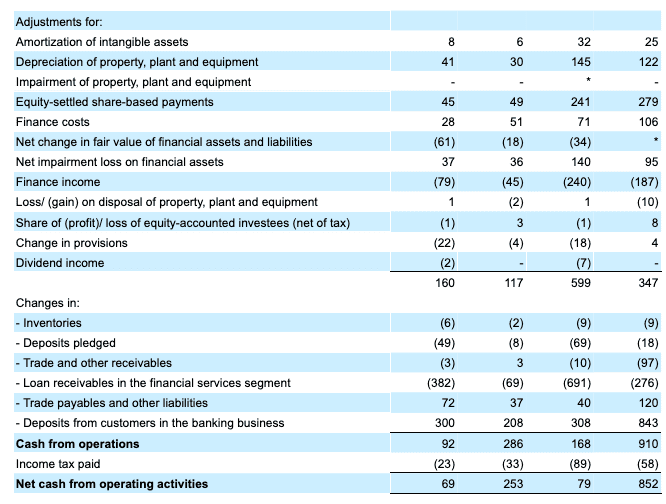

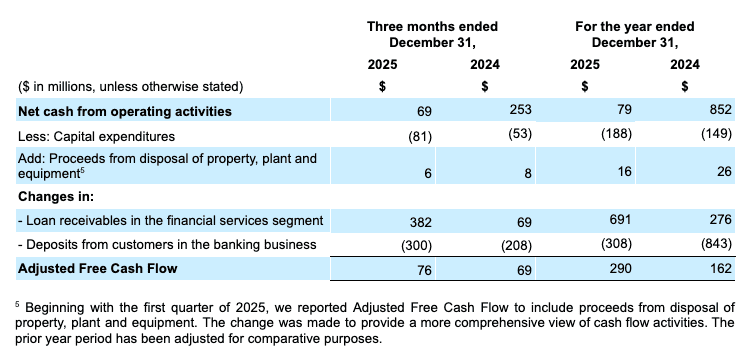

- Net cash from operating activities was $69 million in the fourth quarter of 2025, a decrease of $184 million YoY, due to outflows related to our lending business, partially offset by higher cash inflows from deposits from customers in the banking business and better operating performance. Adjusted Free Cash Flow was $76 million during the quarter, improving by $7 million YoY, and $290 million on a trailing 12-month basis, improving by $128 million YoY. Improvements in Adjusted Free Cash Flow were driven by increasing profitability.

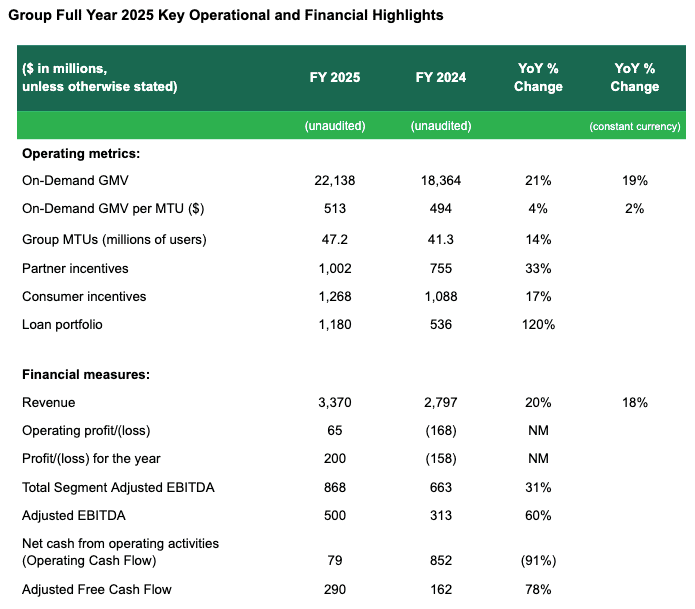

- Revenue for the full year grew 20% YoY, or 18% YoY on a constant currency basis, to a record $3.37 billion as we continued to grow our user base, improve frequency and engagement in the platform, and optimize incentive levels.

- On-Demand GMV grew 21% YoY, or 19% YoY on a constant currency basis, to an all-time high of $22.1 billion, underpinned by strong YoY growth in On-Demand MTUs and a YoY increase in On-Demand GMV per MTU on a constant currency basis.

- Profit for the year was $200 million, a $358 million improvement YoY, driven by improvements in Adjusted EBITDA, increases in net finance income and lower share-based compensation expenses. Non-cash expenses included $241 million in share-based compensation expenses, $177 million of depreciation and amortization and $2 million profit from equity-accounted investees (net of tax).

- Adjusted EBITDA for the full year was $500 million, an increase of $187 million compared to $313 million in 2024.

- Operating Cash Flow was $79 million in 2025, a reduction of $773 million YoY, with higher outflows for loan receivables in the lending business and a smaller increase in deposits from customers, partially offset by improvement in profit/(loss) before income tax.

- Adjusted Free Cash Flow was positive for the full year at $290 million in 2025, compared to $162 million in 2024, mainly driven by improvements in profit/(loss) before income tax.

The above guidance and expected year-over-year growth is primarily attributable to the organic expansion of our business, and represents our expectations as of the date of this press release and may be subject to change.

Segment Financial and Operational Highlights

Deliveries

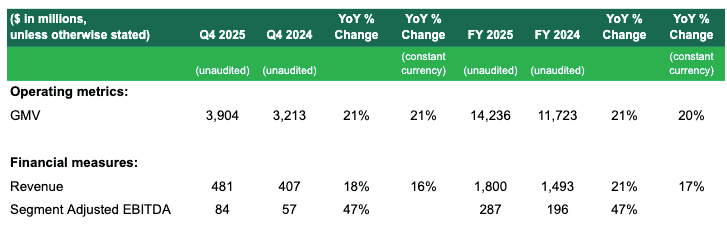

- Deliveries revenue grew strongly by 18% YoY, or 16% YoY on a constant currency basis, to $481 million in the fourth quarter of 2025. For the full year 2025, Deliveries revenue grew 21% YoY, or 17% YoY on a constant currency basis, to $1,800 million. The strong growth was primarily driven by growth in Deliveries GMV and higher contributions from Advertising.

- Deliveries GMV grew strongly by 21% YoY on actual and constant currency basis, to $3,904 million during the quarter, driven by an increase in total Deliveries transactions, MTUs and GMV per MTU. On a full year basis, Deliveries GMV growth accelerated to 21% YoY, or 20% YoY on a constant currency basis, as we continued to broaden our product offerings and drove increased user frequency.

- Deliveries segment adjusted EBITDA margin was 2.2% during the quarter, expanding by 38 basis points from 1.8% in the prior year period. This was primarily driven by growing contributions from our Advertising business and gains in operating leverage. On a full year basis, Deliveries segment adjusted EBITDA margin grew 35bps to 2.0%.

- During the fourth quarter, the total number of quarterly active advertisers who joined our self-serve platform increased 21% YoY to 228,000 while average spend by quarterly active advertisers on our self-serve platform increased 23% YoY, as we continued to deepen Advertising penetration among our merchant-partners.

Mobility

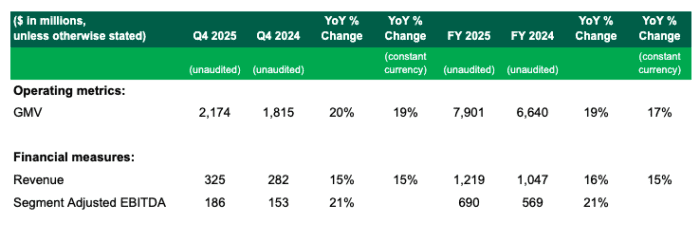

- Mobility revenue grew 15% YoY on an actual and constant currency basis in the fourth quarter of 2025. Growth was underpinned by strong growth in Mobility MTUs as we hit a new all-time high during the quarter as we intentionally continue to drive affordability. For the full year 2025, Mobility revenue grew 16% YoY, or 15% YoY on a constant currency basis, to $1,219 million.

- Mobility GMV grew 20% YoY, or 19% YoY on a constant currency basis, to $2,174 million during the quarter. For the full year 2025, Mobility GMV grew 19% YoY, or 17% YoY on a constant currency basis, to $7,901 million. Mobility transactions grew 27% YoY in 2025, outpacing Mobility GMV growth as we drove greater adoption of our affordable services.

- In the fourth quarter, Mobility segment adjusted EBITDA margin was 8.6%, expanding from 8.4% in the prior year period, primarily driven by greater operating leverage. For the full year 2025, Mobility segment adjusted EBITDA was $690 million, increasing 21% YoY from the prior year period, while Mobility Segment Adjusted EBITDA margin expanded to 8.7%.

Financial Services

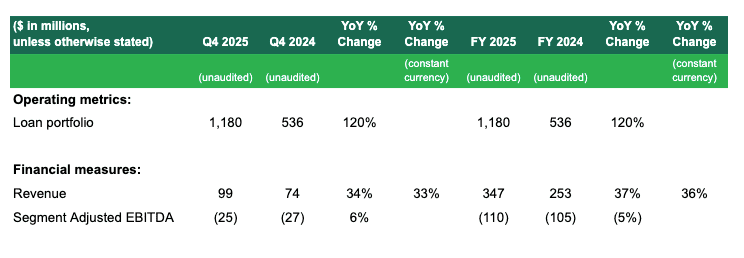

- Financial Services revenue grew 34% YoY, or 33% YoY on a constant currency basis, to $99 million in the fourth quarter of 2025. For the full year 2025, Financial services revenue grew by 37% YoY, or 36% YoY on a constant currency basis, to $347 million. The strong YoY growth was primarily driven by increasing contributions from our lending business.

- Total loans disbursed grew by 53% YoY to $979 million during the fourth quarter. Our net loan portfolio more than doubled YoY to $1,180 million in the fourth quarter from $536 million in the prior year period. Excluding credit loss provisions, our gross loan portfolio was $1,278 million in the fourth quarter, growing from $586 million in the prior year period.

- Financial Services Segment Adjusted EBITDA losses improved by 6% YoY to negative $25 million in the fourth quarter. On a full year basis, Financial Services Segment Adjusted EBITDA losses increased by 5% primarily due to higher credit loss provisions as our loan portfolio continued to scale. We continue to iterate and strengthen our credit risk models to scale our loan portfolio, with 90-days non-performing loans well within our risk appetite and the loan portfolio generating healthy risk-adjusted returns.

- Customer deposits across GXS Singapore and GXBank Malaysia grew to an all-time high of $1.6 billion as of the end of the fourth quarter, compared to $1.2 billion in the prior year period, driven by customer growth, with the majority of depositors also being Grab users.

Others

Other Events

Grab’s Board of Directors has authorized a share repurchase program, under which Grab may repurchase up to $500 million worth of its outstanding Class A ordinary shares. The proposed repurchases may be made from time to time through open market transactions at prevailing market prices, privately negotiated transactions, block trades and/or through other legally permissible means, or any combination thereof, depending on market conditions and the trading price of the Company’s Class A ordinary shares, among other factors, and in accordance with applicable rules and regulations. The Company’s Board of Directors will review the share repurchase program periodically, and may amend the terms and size of the program. The Company intends to fund the repurchases with excess cash after allocating and potentially allocating for investments to drive growth. The share repurchase program does not obligate the Company to acquire any particular amount of Class A ordinary shares.

1 Regional corporate costs are costs that are not attributed to any of the business segments, including certain cost of revenue, research and development expenses, general and administrative expenses and marketing expenses. These regional costs of revenue include cloud computing costs. These regional research and development expenses also include mapping and payment technologies and support and development of the internal technology infrastructure. These general and administrative expenses also include certain shared costs such as finance, accounting, tax, human resources, technology and legal costs. Regional corporate costs exclude share-based compensation expenses and capitalized software costs.

2 Gross cash liquidity includes cash on hand, short-term and long-term time deposits, marketable securities and restricted cash.

3 Net cash liquidity includes gross cash liquidity less loans and borrowings.

4 Adjusted Free Cash Flow Conversion is defined as Adjusted Free Cash Flow as a percentage of Adjusted EBITDA

Forward-Looking Statements

This document and the announced investor webcast contain “forward-looking statements” within the meaning of the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact contained in this document and the webcast, including but not limited to, statements about Grab’s goals, targets, projections, guidances, outlooks, beliefs, expectations, strategy, plans, objectives of management for future operations of Grab, and growth opportunities, are forward-looking statements. Some of these forward-looking statements can be identified by the use of forward-looking words, including “anticipate,” “expect,” “suggest,” “plan,” “believe,” “intend,” “estimate,” “target,” “project,” “should,” “could,” “would,” “may,” “will,” “forecast,” “annualized,” “annualized run-rate,” “on track to” or other similar expressions. Forward-looking statements are based upon estimates and forecasts and reflect the views, assumptions, expectations, and opinions of Grab, which involve inherent risks and uncertainties, and therefore should not be relied upon as being necessarily indicative of future results. A number of factors, including macro-economic, industry, business, regulatory and other risks, could cause actual results to differ materially from those contained in any forward-looking statement, including but not limited to: Grab’s ability to grow at the desired rate or scale and its ability to manage its growth; its ability to successfully execute its growth strategies; its ability to further develop its business, including new products and services; its ability to attract and retain partners and consumers; its ability to compete effectively in the intensely competitive and constantly changing market; its ability to continue to raise sufficient capital; its ability to reduce net losses and the use of partner and consumer incentives, and to achieve profitability; potential impact of the complex legal and regulatory environment on its business; its ability to protect and maintain its brand and reputation; general economic conditions, in particular as a result of currency exchange fluctuations and inflation; expected growth of markets in which Grab operates or may operate; and its ability to defend any legal or governmental proceedings instituted against it. In addition to the foregoing factors, you should also carefully consider the other risks and uncertainties described under “Item 3. Key Information – D. Risk Factors” and in other sections of Grab’s annual report on Form 20-F for the year ended December 31, 2024, as well as in other documents filed by Grab from time to time with the U.S. Securities and Exchange Commission (the “SEC”).

Forward-looking statements speak only as of the date they are made. Grab does not undertake any obligation to update any forward-looking statement, whether as a result of new information, future developments, or otherwise, except as required under applicable law.

Unaudited Financial Information

Grab’s unaudited selected financial data for the three months and year ended December 31, 2025 and 2024 included in this document and the investor webcast is based on financial data derived from Grab’s management accounts that have not been reviewed or audited.

Certain amounts and percentages that appear in this document may not sum due to rounding.

Non-IFRS Financial Measures

This document and the investor webcast include references to non-IFRS financial measures, which include: Adjusted EBITDA, Segment Adjusted EBITDA, Segment Adjusted EBITDA margin, Total Segment Adjusted EBITDA, Adjusted EBITDA margin, Adjusted Free Cash Flow, gross cash liquidity and net cash liquidity. Grab uses Adjusted EBITDA, Segment Adjusted EBITDA, Segment Adjusted EBITDA margin, Total Segment Adjusted EBITDA, and Adjusted EBITDA margin for financial and operational decision-making and as a means to evaluate period-to-period comparisons, and Grab’s management believes that these non-IFRS financial measures provide meaningful supplemental information regarding its performance by excluding certain items that may not be indicative of its recurring core business operating results. For example, Grab’s management uses Total Segment Adjusted EBITDA as a useful indicator of the economics of Grab’s business segments, as it does not include regional corporate costs. Adjusted Free Cash Flow excludes the effects of the movement in working capital for our lending and digital banking deposit activities. Grab uses Adjusted Free Cash Flow to monitor business performance and assess its cash flow activity other than its lending and digital banking deposit activities, and Grab’s management believes that the additional disclosure serves as a useful indicator for comparison with the cash flow reporting of certain of its peers. Grab uses gross cash liquidity and net cash liquidity to assess our ability to meet short-term obligations and invest in growth opportunities.

However, there are a number of limitations related to the use of non-IFRS financial measures, and as such, the presentation of these non-IFRS financial measures should not be considered in isolation from, or as an alternative to, financial measures determined in accordance with IFRS. In addition, these non-IFRS financial measures may differ from non-IFRS financial measures with comparable names used by other companies. See below for additional explanations about the non-IFRS financial measures, including their definitions and a reconciliation of these measures to the most directly comparable IFRS financial measures. With regard to forward-looking non-IFRS guidance and targets provided in this document and the investor webcast, Grab is unable to provide a reconciliation of these forward-looking non-IFRS measures to the most directly comparable IFRS measures without unreasonable efforts because the information needed to reconcile these measures is dependent on future events, many of which Grab is unable to control or predict.

Explanation of non-IFRS financial measures:

- Adjusted EBITDA is calculated as profit (loss) for the period adjusted to exclude: (i) net finance income (costs), including interest income (expenses), foreign exchange gain (loss) and changes in fair value of financial assets and liabilities, (ii) net other income (expenses), (iii) income tax expenses (credit), (iv) depreciation and amortization, (v) share-based compensation expenses, (vi) costs related to mergers and acquisitions, (vii) impairment losses on goodwill and non-financial assets, (viii) restructuring costs, (ix) legal, tax and regulatory settlement provisions, and (x) other items not indicative of our ongoing operating performance.

- Segment Adjusted EBITDA represents the Adjusted EBITDA of each of our four business segments, excluding, in each case, regional corporate costs.

- Segment Adjusted EBITDA margin is calculated as Segment Adjusted EBITDA divided by Gross Merchandise Value. For Financial Services and Others, Segment Adjusted EBITDA margin is calculated as Segment Adjusted EBITDA divided by Revenue.

- Total Segment Adjusted EBITDA represents the sum of Adjusted EBITDA of our four business segments.

- Adjusted EBITDA margin is calculated as Adjusted EBITDA divided by Revenue.

- Adjusted Free Cash Flow is defined as net cash flows from operating activities less capital expenditures (including assets acquired under lease arrangements), plus proceeds from disposal of property, plant and equipment, and excluding changes in working capital related to loans and advances to customers, and deposits from the digital banking business.

- Gross cash liquidity includes cash on hand, short-term and long-term time deposits, marketable securities and restricted cash.

- Net cash liquidity includes gross cash liquidity less loans and borrowings.

We compare the percent change in our current period results from the corresponding prior period using constant currency. We present constant currency growth rate information to provide a framework for assessing how our underlying GMV and revenue performed excluding the effect of foreign currency rate fluctuations. We calculate constant currency by translating our current period financial results using the corresponding prior period’s monthly exchange rates for our transacted currencies other than the U.S. dollar.

Operating Metrics

Gross Merchandise Value (GMV) is an operating metric representing the sum of the total dollar value of transactions from Grab’s products and services, including any applicable taxes, tips, tolls, surcharges and fees, over the period of measurement. GMV includes (i) sales made through offline stores reported under the deliveries segment; and (ii) revenues made from products and services provided to driver-partners, merchant-partners and other customers to support their businesses, such as GrabAds and GrabRentals, reported under the deliveries and/or mobility segment, as applicable. Mobility GMV is an operating metric representing the GMV of our Mobility segment. Deliveries GMV is an operating metric representing the GMV of our Deliveries segment. On-Demand GMV is an operating metric defined as the sum of Mobility GMV and Deliveries GMV. GMV is a metric by which Grab understands, evaluates and manages its business, and Grab’s management believes is necessary for investors to understand and evaluate its business. GMV provides useful information to investors as it represents the amount of customer spend that is being directed through Grab’s platform. This metric enables Grab and investors to understand, evaluate and compare the total amount of customer spending that is being directed through its platform over a period of time. Grab presents GMV as a metric to understand and compare, and to enable investors to understand and compare Grab’s aggregate operating results, which captures significant trends in its business over time.

Monthly Transacting User (MTUs) is defined as the monthly number of unique users who transact via Grab’s apps, where transact means to have successfully paid for or utilized any of Grab’s products or services (including lending and offline Jaya Grocer transactions where users record their Jaya Grocer loyalty points on the Grab app). MTUs over a quarterly or annual period are calculated based on the average of the MTUs for each month in the relevant period. MTUs is a metric by which Grab understands, evaluates and manages its business, and Grab’s management believes is necessary for investors to understand and evaluate its business.

Partner incentives is an operating metric representing the dollar value of incentives granted to driver- and merchant-partners, the effect of which is to reduce revenue. For certain delivery offerings where Grab is contractually responsible for delivery services provided to end-users, incentives granted to driver-partners are recognized in cost of revenue.

Consumer incentives is an operating metric representing the dollar value of discounts and promotions offered to consumers, the effect of which is to reduce revenue. Partner incentives and consumer incentives are metrics by which we understand, evaluate and manage our business, and we believe are necessary for investors to understand and evaluate our business. We believe these metrics capture significant trends in our business over time.

Loan portfolio is an operating metric representing the total of current and non-current loan receivables in the financial services segment, net of expected credit loss allowances.

Industry and Market Data

This document may contain information, estimates and other statistical data derived from third party sources, including research, surveys or studies, some of which are preliminary drafts, conducted by third parties, information provided by customers and/or industry or general publications. Such information involves a number of assumptions and limitations due to the nature of the techniques and methodologies used in market research, and as such neither Grab nor the third-party sources can guarantee the accuracy of such information. You are cautioned not to give undue weight to such estimates. Grab has not independently verified such third-party information, and makes no representation as to the accuracy of such third-party information.

Impact of $1.5 Billion Convertible Notes Offering on Reported Financial Results

The conversion feature within the convertible notes is accounted for as a derivative liability under IFRS, with its fair value re-measured each reporting period. While this generates volatility in profit/loss, it does not impact Grab’s underlying cash flows or adjusted EBITDA.

Unaudited Summary of Financial Results

Condensed consolidated statement of profit or loss and other comprehensive income

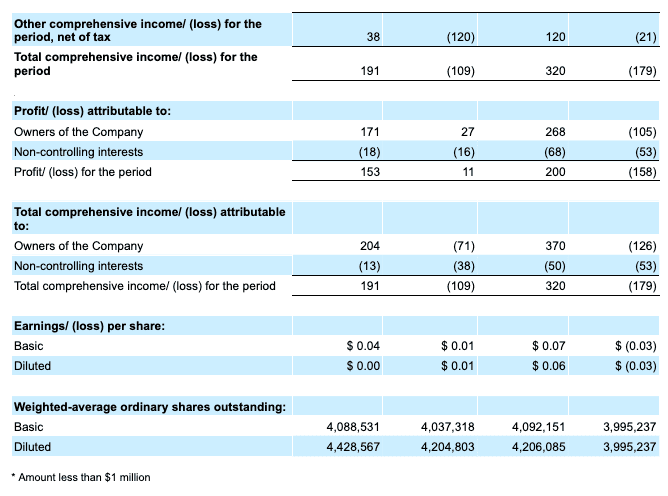

The number of outstanding Class A and Class B ordinary shares was 3,969 million and 120 million as of December 31, 2025, and 3,950 million and 115 million, respectively, as of December 31, 2024. Additionally, 269 million and 222 million potentially dilutive securities have been considered for the computation of diluted earnings per ordinary share for the year ended December 31, 2025 and 2024, respectively.