Key takeaways:

- There are two commonly used methods for calculating returns; Time-Weighted Return (TWR) and Money-Weighted Return (MWR).

- Time-weighted calculations reflect your investment strategy and do not take into account the impact of cash flows in and out of your portfolio.

- Money-weighted calculations reflect your returns for your personal investment portfolio and do take into account the impact of cash flows in and out of your portfolio.

- GrabInvest uses the MWR method as it is an easier way of evaluating your portfolio performance.

It is natural to be curious about the performance of your investment; after all, you invested your hard earned money! Counting dollars and cents is easy but when it comes to investment portfolios…things become more technical.

There are different methods to calculate portfolio performance and depending on the method used it will affect the reflection of % returns. The two methods of calculating returns are Time-Weighted Returns (TWR) and Money-Weighted Returns (MWR). At GrabInvest we use the MWR method. Not sure what that means? No problem, let us explain.

What are TWR and MWR?

While the method used to calculate returns won’t have a massive impact on your day-to-day investing, it will impact the way your % return is reflected and so it can be helpful to understand the different methods of calculating returns and what this means for you when you check your portfolio.

Both time-weighted and money-weighted methods are useful ways to calculate returns, but they approach calculations differently and can have differing outcomes for reflecting % returns.

Time-Weighted Returns = return on my investment strategy

Time-weighted returns are calculated on a daily basis and pay attention to when a return was generated and what the invested amount was. This method eliminates the impact of cash flows into and out of the portfolio and so it is a useful metric for comparing portfolios. However, it is less intuitive as changes in your total investment will cause a change in the reflection of returns %.

Money-Weighted Returns = return on my investment portfolio

Money-weighted returns are calculated over the average invested balance during the period. It does not matter at what point within the period the returns were generated. The simpler setup makes this method more intuitive and easier to follow and can provide insight into the effectiveness of investment decisions.

Good saving and investing habits will see money being allocated to your portfolio periodically. When the total invested amount is expected to change frequently, it is advantageous to use the money-weighted method to intuitively understand your portfolio performance.

TWR vs MWR; how do they compare?

There are certain situations when MWR and TWR are identical and reflect the exact same % return. This happens when there are no new investments or withdrawals from the portfolio after the first investment.

Most of the time, however, the % returns will be different. This happens when you hold different investment amounts in your portfolio at different points in time of the strategy.

- Maybe you hold less money in the portfolio when strategy returns are high and more money when the strategy returns are low. In that case your portfolio returns (Money-Weighted Returns) would be lower than the strategy returns (Time-Weighted Returns).

- Maybe you hold more money in the portfolio when strategy returns are high and less money when the strategy returns are low. In that case your portfolio returns (Money-Weighted Returns) would be higher than the strategy returns (Time-Weighted Returns).

Here are some examples of both TWR and MWR at work.

Imagine a portfolio that holds $100 for one month and generates a return of $1. Since there are no new investments or withdrawals from the portfolio, both the TWR and the MWR methodologies come to the same outcome of a 1% return.

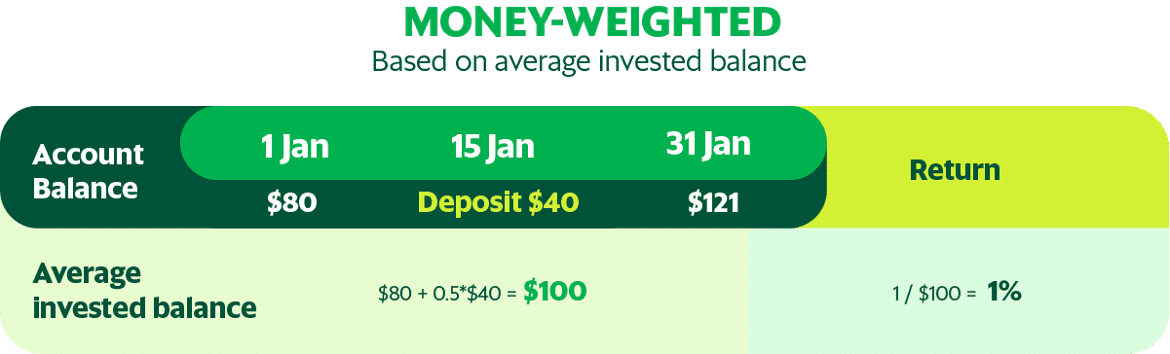

Now, let’s imagine that this portfolio starts with $80 at the beginning of the month, and half way through the month receives an additional $40 in investment to an invested balance of $120. The portfolio also generates a return of $1 during this month.

The MWR method is based on the average invested balance, which is still $100. In the first half of the month you have $80 invested. In the second half of the month you have $120 invested. Therefore, the average invested for the month is $100. You take $80+$120 and divide it by 2 (being: $80 + 0.5 * $40), and therefore results in $1 return / $100 average invested balance = 1% return.

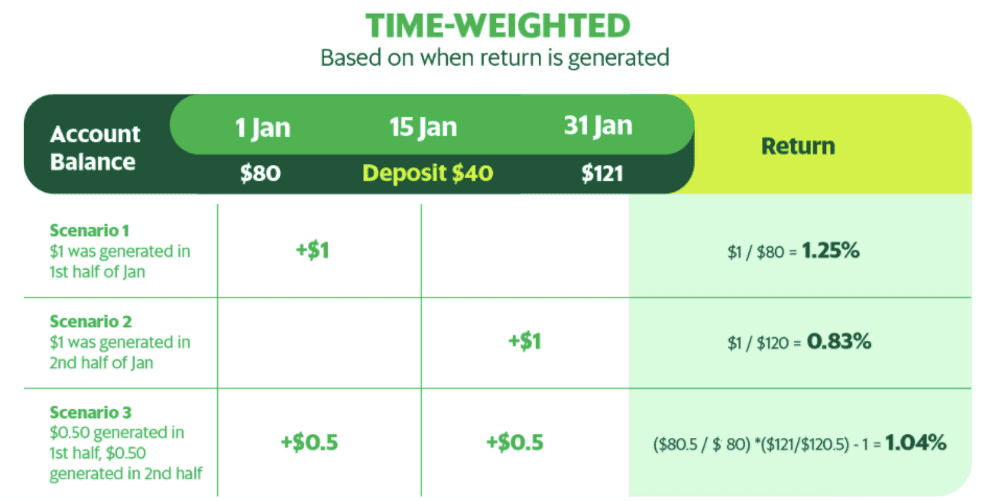

For the TWR method, the % return you see generated is dependent on the amount of invested balance you have when you start calculating the return. If the $1 return was generated and thus calculated at the start of the month with $80 capital, the % return will be $1.25%. However, If the $1 return was generated and calculated at the end month with a $120 invested balance, the % return will be 0.83%. Therefore, even if it seems like return performance has dipped, the absolute return is still $1. We still use the same portfolio that starts the month with $80 and receives an additional $40 halfway through the month. So the average invested balance is $100.

a) Scenario 1: If the $1 was generated in the first half of the month when the invested balance was $80, then the return for the whole month is $1 / $80 = 1.25%.

b) Scenario 2: If the $1 was generated in the second half of the month when the invested balance was $120, then the return for the whole month is $1$ / $120 = 0.83%.

c) Scenario 3: If $0.5 of the return was generated in the first half of the month and the remaining $0.5 was generated in the second half, then the outcome is 1.04% (being: ($80.5 / $80) * ($121 / $120.5) – 1).

The MWR method is often more intuitive for end investors since fewer input numbers are needed. The TWR method is highly dependent on the exact daily path of flows and returns but can provide outputs that can be compared across different strategies.

While both methods are useful, at GrabInvest, we believe that a money-weighted approach is optimal for analysing the true performance of your investment portfolio. Regardless of which method is used to calculate returns, it is important to remember that the % return only tells a small part of a much bigger story.