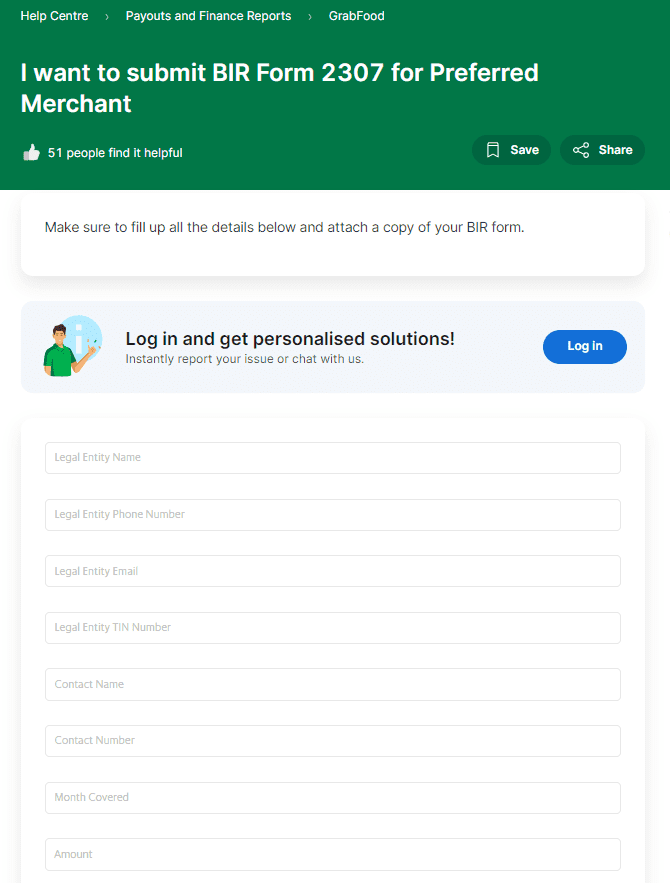

HOW TO SUBMIT THE REQUIREMENTS?

Here’s the step-by-step guide on how you can easily submit the requirements that are requested:

STEP 1: Click here to submit your requirements. Kindly fill out the form with your required information.

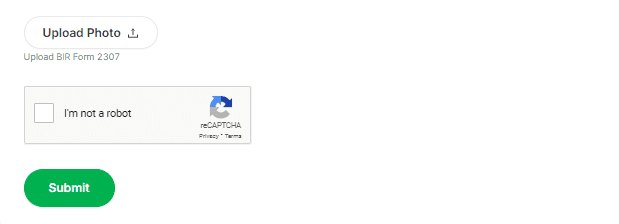

STEP 2: Upload your documents (make sure to name your documents as Certificate of Registration (COR) , BIR Form 2303, and Sworn Declaration). Click “Submit”.

Please expect your respective Account Managers to contact you to explain further. If you do not have assigned Account Manager, kindly visit our Merchant Help Center for Grab-specific inquiries or concerns.

Kindly wait for further announcement regarding the new process of the BIR 2307 release.